Global share markets rose over the last week helped by optimism that a US debt ceiling deal will soon be reached and with economic data still holding up. Despite a messy session on Friday, with US shares initially up with Fed Chair Powell signalling an inclination to pause on rates and then falling to end down 0.1% as debt ceiling talks paused over an impasse on spending cuts, for the week US shares gained 1.7%. Over the week Eurozone shares rose 1.3%, Japanese shares rose 4.8% to their highest since 1990 and Chinese shares rose 0.2%. Supported by the positive global lead Australian shares rose by 0.3% with gains in IT and resources shares offsetting weakness in retailers, health and property stocks. However, bond yields rose globally and in Australia with the local money market now pricing in the RBA holding in June but a 64% probability of another 0.25% RBA rate hike by September. Oil and iron ore prices rose but metal prices were flat to down. The $A was little changed as the $US rose.

While shares could have a further tactical bounce if there is quick US debt ceiling deal, they continue to look vulnerable over the next few months. From their lows last year global and US shares are up 17% and Australian shares are up 13% as investors have been buoyed by evidence of peaking inflation, anticipation that central banks are near the top and so far resilient growth and profits. However, we remain of the view that global and Australian share markets are vulnerable to a rougher period ahead: share market gains so far have been narrowly based favouring defensive sectors than would be normal at this point in a recovery; US debt ceiling brinkmanship and eventual resolution could create volatility ahead; banking stress is continuing in fits and starts in the US resulting in additional monetary tightening; leading economic indicators continue to point to a high risk of recession in the US and Australia; China’s recovery is looking less robust; metal and energy prices have softened with oil down despite several OPEC supply cuts suggesting weakening demand; central banks are probably close to the top but risk doing more; and the period from May to September is often rough for shares. We remain of the view that shares will do okay on a 12 month view as central banks ease up but the next few months are likely to be rough.

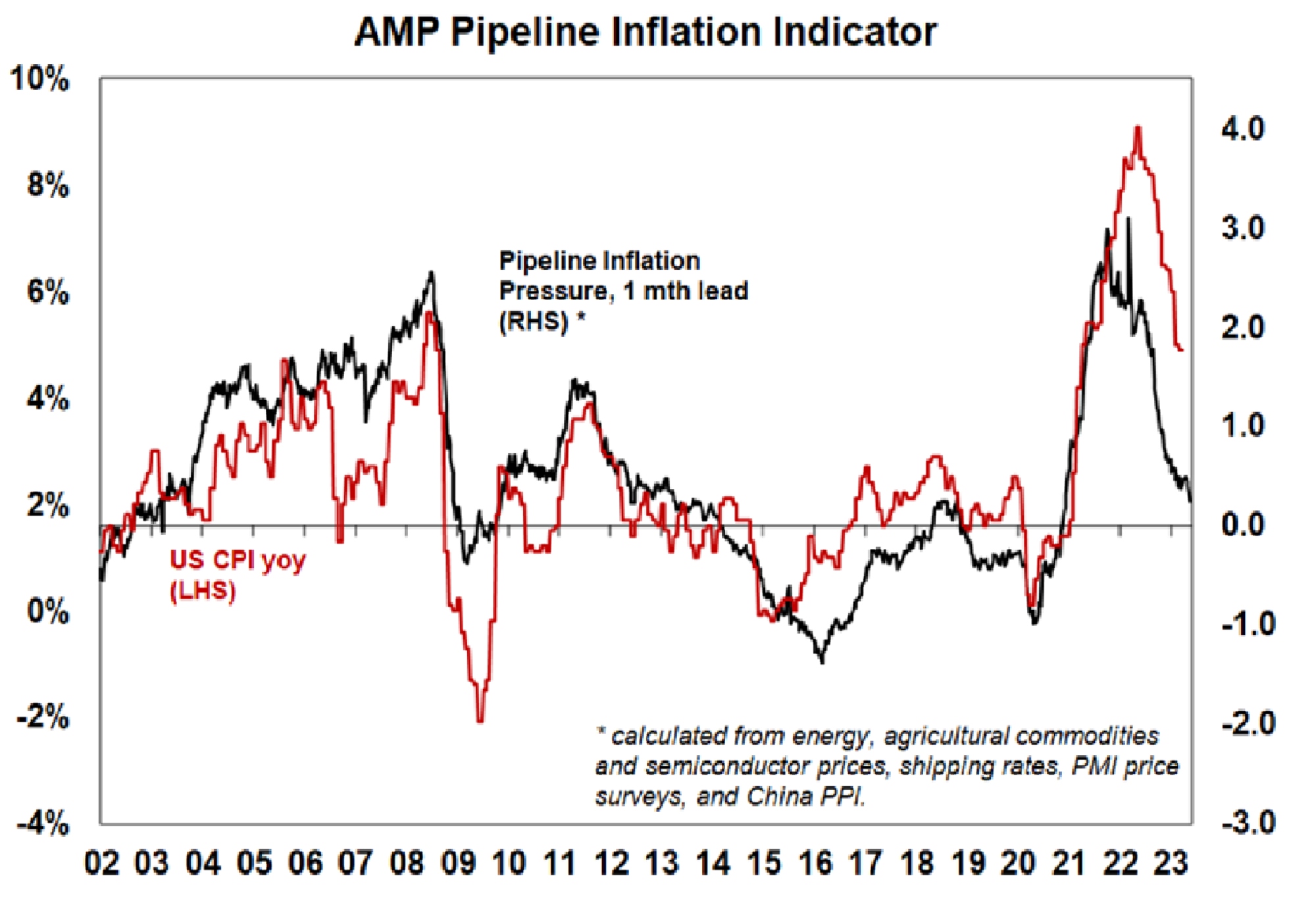

The good news though is that our US Pipeline Inflation Indicator is continuing to fall pointing to a further fall in US inflation ahead. This will ultimately support central bank rate cuts, and then share markets on a 12-month view.

Source: Bloomberg, AMP

US debt ceiling negotiations appear to be heading in the right direction, but as we saw Friday there could still be a few setbacks along the way. A failure to raise the debt ceiling would mean that US Government spending will have to be slashed by around 7% of GDP (ie to bring spending back into line with revenue) which means the US “defaulting” on some of its spending or debt servicing commitments and this would likely drive a US recession and financial market turmoil with a flow on to Australia. However, we have seen this movie before, and default is not the most likely outcome as the US political leadership on both sides of politics (Trump excepted) don’t want to be seen as responsible for recession and default ahead of next year’s elections. That said we would put the risk of default at 15% reflecting more fiscally conservative Republicans in Congress now who want big spending cuts (although I am not entirely sure much has changed since the Tea Party days a decade ago), ie its a significant risk but not the base case. Here are the key points:

- Although Treasury Secretary Yellen has put the X date when the US Government runs out of spare cash at around 1 June, if it manages to scrape through to mid-June it will benefit from quarterly tax payments which could see it hang on to early August. But slowing revenue flows have increased the risk that its early June. Increasing the debt ceiling by June 1 will require a deal very quickly so it can get passed in Congress.

- President Biden doesn’t want to cut spending as it will add to recession risk ahead of next year’s presidential election and go down badly with progressive Democrats. But Republican’s want to try and slow the economy down. So some sort of compromise will be required.

- So far things seem to be heading in the right direction for an eventual resolution: following Yellen’s warning that the X date may be 1 June both sides are taking it seriously; negotiations have started with negotiators narrowed down to those who can make decisions for Biden and House Speaker McCarthy; any deal will involve spending caps of some sort and other tradeoffs (like energy permits and work for welfare requirements); Biden and McCarthy have expressed confidence and both the House and Senate are reportedly making plans for votes on it in the coming days suggesting Biden is open to some spending cuts; but neither side will want to be seen as agreeing too easily as it will go badly with their base; so as we saw Friday, with talks briefly pausing as McCarthy complained about the White House resisting spending cuts, the risk of more setbacks and brinkmanship is high until a deal is worked out in the 11th hour possibly requiring a mini-share market panic to get it over the line; an extension of the debt ceiling may come but probably only to buy time to finalise a deal and pass it through Congress.

- Raising the debt ceiling may provide short term relief for share markets but they are vulnerable to spending cuts adding to the risk of recession and the US Treasury reversing the liquidity boost it’s been providing lately by running down its cash reserves at the Fed. In the 2011 debt ceiling debacle the US share market fell 4% ahead of the deal to raise the debt ceiling but 13% afterwards.

In Australia, we continue to see the RBA holding rates at 3.85% at its June meeting, but further rate hikes remain a high risk. The minutes from the last RBA board meeting reiterated that further rate hikes may still be required depending on economic activity and inflation data. Looking at the data since the last meeting: business conditions remain solid but are slowing; retail sales have been soft; wages growth has increased a bit further but is in line with RBA forecasts and there are no signs of a wages breakout; and April jobs data came in weaker than expected with an emerging rising trend in unemployment. Of course, there is still retail sales data (26 May) and inflation data (31 May) to come but so far the data flow since the last meeting suggests that the RBA should leave rates on hold at its June meeting in order to better assess the impact of past rate hikes and avoid unnecessarily plunging the economy into recession. We think that further tightening would be overkill, but with the RBA minutes reiterating the Bank’s concerns about sticky services inflation, the tight labour market, the risk of rising inflation expectations, weak productivity growth and the increase in home prices the risk of further rate hikes is very high.

The problem with economic data following interest rate hikes is that “it’s ok till it isn’t”. We saw this in the late 1980s when the RBA kept jacking up interest rates in 1988 and 1989 with the economy remaining resilient and fuelling more rate hikes…until the economy fell into recession in 1990. Inflation and unemployment are lagging indicators so running interest rates mostly looking at them is like driving the car with the rear-view mirror and runs the high risk of an accident.

Active quantitative tightening under consideration by the RBA. Interestingly the Bank also indicated that it was open to a move at some point from passive quantitative tightening (ie letting its balance sheet run down as bonds mature and Term Funding Facility loans are repaid) to actively selling down its bond holdings given that its large bond holdings expose it to significant interest rate risk. While a move is not imminent a shift to active quantitative tightening could add to the risk of overtightening, particularly with the risk of still further interest rate hikes.

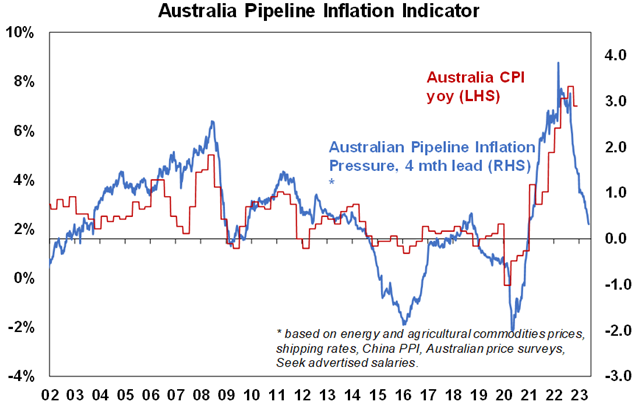

Out of interest, our Australian Pipeline Inflation Indicator is continuing to fall pointing to sharp fall in inflation ahead. Its now coming down as quickly as it went up suggesting that inflation could surprise the RBA on the downside.

Source: Bloomberg, AMP

Imagine a great big melting pot to solve many of the world’s problems. In the late 1960s and early 1970s it seemed that many, observing cultural and racial difference as a source of the world’s social problems, envisaged a world where such differences were no more. John Lennon’s Imagine, imagined a world where “there’s no countries…nothing to kill or die for and no religion too…[where] the world will live as one”. Blue Mink’s Melting Pot (which unfortunately contained some inappropriate words that weren’t meant to be insulting or racist but unfortunately distract today from the song’s anti-racist sentiment) wanted to mix the world’s races in “a great big melting pot” and “turn out coffee coloured people” for a “get along scene”. Many conservatives at the time would have been aghast at such progressive ideas, although many progressives may now see such sentiments as naïve and insensitive to difference.

Economic activity trackers

Our Economic Activity Trackers rose slightly in the Australia and Europe, but the US fell further. Overall, they are suggesting flat to only slightly positive economic growth year to date in Australia and Europe, but possibly an emerging contraction in the US.

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence, credit & debit card transactions and hotel bookings. Source: AMP

Major global economic events and implications

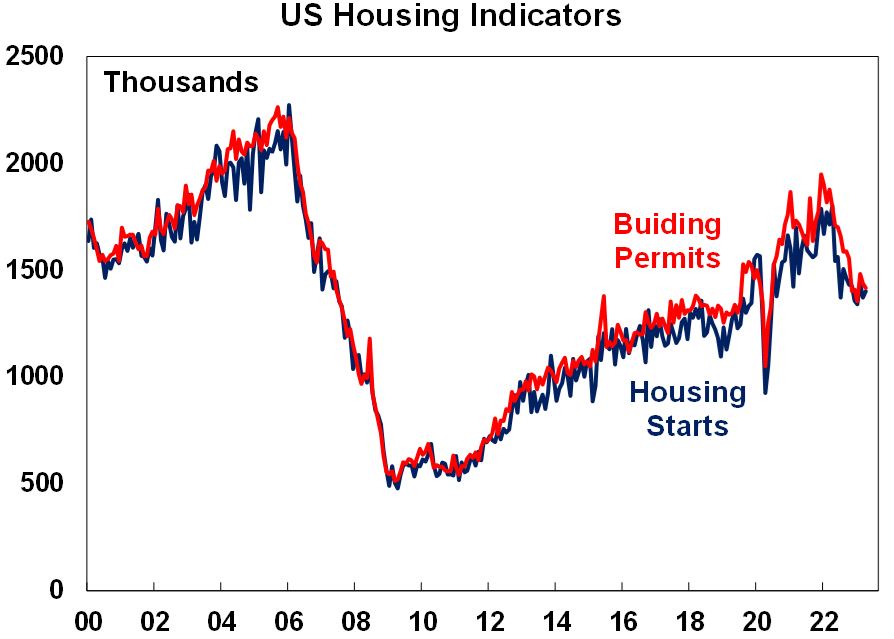

US economic data was mixed again. The NAHB’s home building conditions survey continued its recent recovery, housing starts rose but permits to build new homes fell and both are well down from their highs and existing home sales fell. Underlying retail sales and industrial production rose more than expected in April although the trend in both is soft. Jobless claims fell but the trend remains up. The US leading index fell again in May and is down 8%yoy which is warning of a high risk of recession. Manufacturing conditions in the New York and Philadelphia regions moved in different directions but both are weak. The surveys’ prices received components fell and are averaging around pre inflation spike levels. Meanwhile Fed Chair Powell signalled an inclination to pause rate hike at the Fed’s June meeting noting that “having come this far, we can afford to look at the data and the evolving outlook to make careful assessments.”

Source: Macrobond, AMP

Source: Macrobond, AMP

Canadian inflation rose in April to 4.4%yoy, up from 4.3% leading to increased expectations that the BoC will raise rates again with markets pricing in roughly a 50% chance of another 0.25% rate hike. However, underlying inflation measures fell further to 4.2%yoy suggesting inflationary pressures are still easing.

Stronger than expected growth in Japan. Japanese March quarter GDP came in stronger at 0.4%qoq or 1.3%yoy driven by strength in consumer spending, business investment and public investment. Inflation also accelerated to 3.5% in April with core (ex food and energy) inflation rising to 2.5% from 2.3%, partly due to rising lodging costs as travel subsidies were terminated.

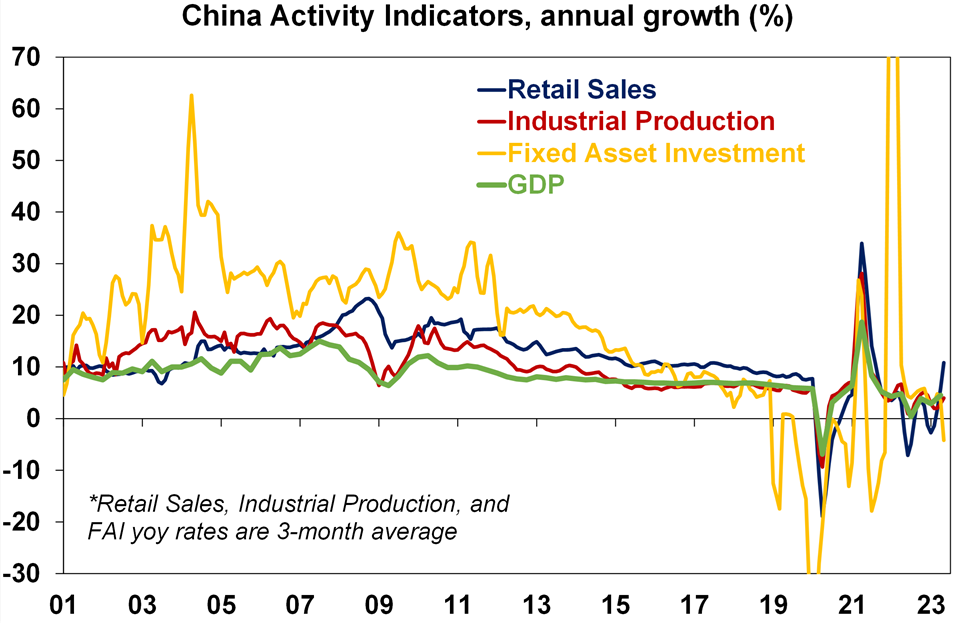

China’s recovery looks to be losing some momentum. Chinese economic activity data for April was softer than expected. Retail sales growth accelerated to 18.4%yoy but this was due to base affects associated with lockdowns a year ago with sales actually down 7.8% in April. Industrial production growth rose but by less than expected and investment growth slowed. While residential property sales are turning up and home prices are continuing to rise, residential investment remains weak. Unemployment was little changed at 5.2% but youth unemployment rose to a new record high of 20.4%. Overall, it appears momentum from the reopening may have faded quicker than in other countries (partly due to less support for the household sector and so less pent up saving) and further policy easing may be required.

Source: Bloomberg, AMP

Australian economic events and implications

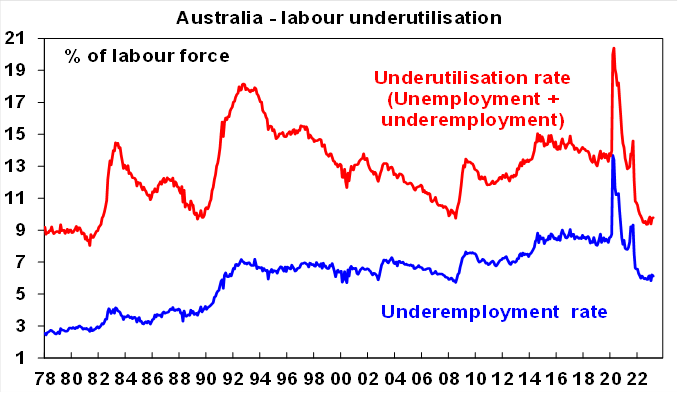

In Australia, jobs data for April was soft with employment down slightly and unemployment rising to 3.7%, up from a low of 3.4% and labour market underutilisation edging up to 9.8%. While the jobs market is still tight with unemployment still around its lowest in nearly 49 years, it does appear to be slowing.

Source: ABS, AMP

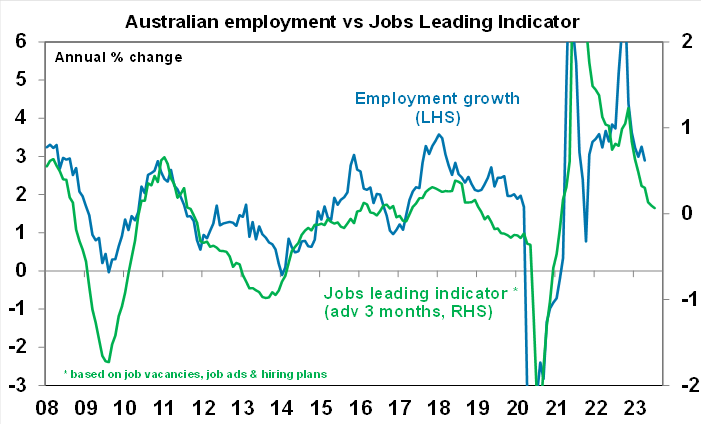

Forward looking indicators for the jobs market point to a slowdown. This is evident in our Jobs Leading Indicator which is based on job vacancies, job ads and business hiring plans.

Source: ABS, AMP

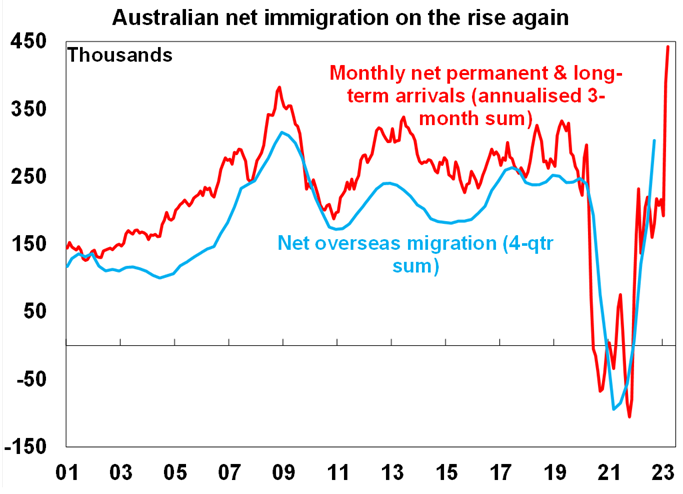

Surging immigration to cool the jobs market but heat up the property market. Monthly net permanent and long term arrivals data to Australia up to March has now pushed above an annualised 400,000 pointing to a continuing surge in Australia’s population. This has pushed working age population growth up to 2.4%yoy (from 1.6%yoy pre pandemic) and will help fill job vacancies and cool the jobs market. But it will also add to the already tight housing market continuing upwards pressure on rents and (mostly indirectly) home prices.

Source: ABS, AMP

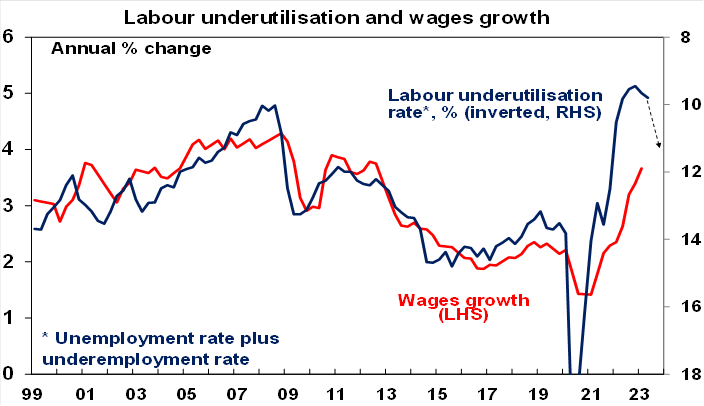

Wages growth continuing to accelerate, but still no wages breakout (yet). March quarter wages growth rose a slightly weaker than expected 0.8%qoq taking annual growth with upwards revisions to a slightly stronger than expected 3.7%yoy. This was the fastest annual increase since 2012. This is a long way from a wages break out, roughly in line with RBA forecasts and (provided productivity growth improves) is roughly consistent with the RBA’s 2-3% inflation target. As such it doesn’t add to the case for another rate hike on its own. While wages growth is likely to rise a bit further a weakening jobs market is likely to see it level off over the next year. However, there are still some aspects that will keep the RBA worrying about a wages breakout: there is a rising share of jobs with bigger wage rises; public sector wages growth is likely to rise further with the lift in some public sector wage caps; a minimum wage increase around 7% (which will impact around 22% of the workforce) along with the 15% wage rise for aged care workers (with a likely flow on to hospitality workers) could substantially add to overall wages growth. So while it doesn’t provide a smoking gun for a rate hike next month, the RBA will likely still see the risks to wages growth as being on the upside such that the risk to the cash rate is on the upside.

Source: ABS, AMP

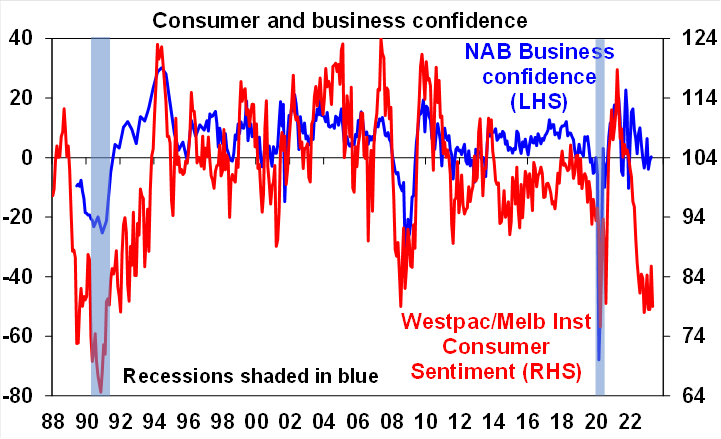

Consumer confidence back to its lows. Highlighting the soft economic outlook consumer confidence fell back to around its lows this month reflecting the latest RBA rate hike and not helped by the absence of handouts for most Australians in the Budget. It continues to remain well below business confidence and warns of softer conditions ahead as the reopening boost and pent up demand wears off.

Source: Westpac/MI, NAB, AMP

What to watch over the next week?

Business conditions PMIs for April for the US, Europe, Japan and Australia will be released on Tuesday and will be watched for a slowing in growth after strength in the last few months and further signs of easing inflation pressures.

In the US, the Fed will release the minutes from its last meeting (Wednesday) which will likely affirm a substantial easing in its tightening bias and greater data dependency. On the data front expect a fall in new home sales (Tuesday), a further slight fall in core private financial consumption deflator inflation for April to 4.5%yoy from 4.6% in March and soft durable goods orders (both due Friday).

The RBNZ (Wednesday) is expected to raise its cash rate again by 0.25% taking it to 5.5%.

In Australia, expect a 0.1% fall in retail sales for April (Friday) confirming that higher interest rates and cost of living pressures are continuing to impact household spending.

Outlook for investment markets

The next 12 months are likely to see easing inflation pressures, central banks moving to get off the brakes. This along with improved valuations should make for reasonable share market returns in contrast to 2022. But the next few months may be rough given high recession and earnings risks, uncertainty around US banks and raising its debt ceiling, geopolitical risks and poor seasonality out to around September/October. This is likely to impact both global and Australian shares.

Bonds are likely to provide returns above running yields, as growth and inflation slow and central banks become less hawkish.

Unlisted commercial property and infrastructure are expected to see slower returns, reflecting the lagged impact of last year’s rise in bond yields on valuations. Commercial property returns are likely to be negative as “work from home” hits space demand as leases expire.

With an increasing supply shortfall, we have revised up our national average home price forecast for this year from a fall of -7% to around flat to up slightly ahead of 5% growth next year. However, the risk a further leg down putting us back on track for a 15-20% top to bottom fall on the back of the impact of high interest rates and higher unemployment are very high (at around 45%) with the latest RBA hike adding to that risk.

Cash and bank deposits are expected to provide returns of around 3.5%, reflecting the back up in interest rates.

A rising trend in the $A is likely over the next 12 months, reflecting a downtrend in the overvalued $US and the Fed moving to cut rates.